Taiwan, Malaysia most affected by US tariffs on Chinese goods, says Schroders

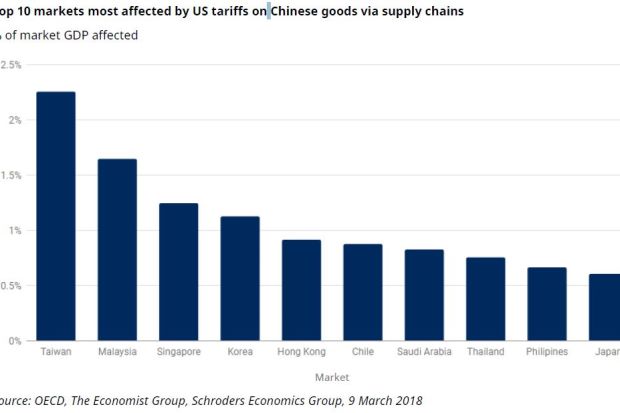

KUALA LUMPUR: Taiwan, Malaysia and Singapore are among the top 10 markets most affected by US tariffs on Chinese goods via the supply chain as US President Donald Trump raised the rhetoric in the trade war against China, says Schroders.

In a report issued on Wednesday, Schorder said tariffs on Chinese exports are much more consequential for emerging market (EM) economies than those on US exports, and that the pain is likely to be concentrated in Asian EM.

“Many economies and companies outside the US and China could be exposed because of their interconnected supply and revenue chains, potentially putting global economic growth at risk,” said emerging markets economist Craig Botham.

He said the US and China have been trading fierce rhetoric over the past two months, threatening to slap billions of dollars’ worth of tariffs on each other’s goods and services.

“While the current dispute between the two economies hasn’t officially been classified as a trade war the threat is real,” he said.

Botham pointed out that headlines have focused on the damage to China in the event of any trade war, but other EM economies could suffer almost as much.

In some cases, governments in those other economies will lack the resources of Beijing, and will face greater domestic political pressure to act.

“There could be some economies less exposed to the first-round effects of tariffs; the immediate damage is focused chiefly on EM Asia, while relatively closed economies such as Brazil and India should be more insulated than other economies in the event of a more global trade war,” he said.

Commenting on the impact on the stockmarkets, Botham said market performance since steel and aluminium tariffs were announced suggests only limited concern about trade tensions, with the global index grinding higher.

However, compared to performance in 2017, gains this year have generally been mediocre, and much more volatile.

“Markets are perhaps not yet convinced that a trade war is inevitable, but they are equally uncertain that it can be avoided,” he said.

There are of course multiple factors at work. The weakness in Chinese markets could be driven also by tighter credit conditions and concerns over slower growth, for example. There have also been doubts over the pace of global expansion which have weighed on equity sentiment.

Nonetheless, trade concerns do seem to be taking some toll. For now the market seems to be betting that a trade war between China and the US can be avoided, but a glance at the Mexican stock exchange tells us that trade tensions can take a real toll when they intensify.

On the possible winners from a trade war, he highlighted that China and the US will need to replace supplies of impacted goods given the cost increase; as reflected by a surge in the price of Brazilian soya beans since China proposed a 25% tariff on imports of the produce from the US.

Not all areas have the potential for significant gains; US whisky exports to China were around US$6mil in 2016, a tiny fraction of any market’s GDP.

“Still, the potential for increased market share elsewhere is meaningful.

“China’s tariffs on US goods will mainly offer opportunities to developed market economies who could look to replace the US as a major supplier of higher value-added commodities, while other EM economies will hope to substitute for China as a provider of raw materials and components,” he said.

On the fallout from the tariffs on consumers, he said the immediate price impact for US consumers should be limited.

In general the US has avoided targeting consumer goods, so most of the effects will come through increased production costs for US firms.

Ultimately, pricing power for companies seems somewhat constrained so this could limit the degree of how much is passed through.

“One possible exception to this is the more recent threat from President Trump to impose a 25% tariff on vehicle imports, which would translate immediately into price increases for the end user.

“On top of possible price increases, it seems likely that tariffs would weigh on growth. Producers unable to pass on cost increases, for example, will generate less profit and so could choose to reduce production. On a large enough scale, this could ultimately filter through to reduced growth in employment and wages,” he said.

Source: The Star

Photo Credit: The Star